.svg)

Belgian Tech H1 2026: The Series A Gap Is Closing, a Bigger One Is Opening

For years, the story of Belgian tech had one recurring villain: the Series A gap. Founders raised a seed, built something real, then often hit a wall when it came time to raise the round that turns a promising company into a scaling one.

The H1 2026 figures come from research produced with Agoria and Scaleup Flanders, our partners on the State of Belgian Tech this year.

.svg)

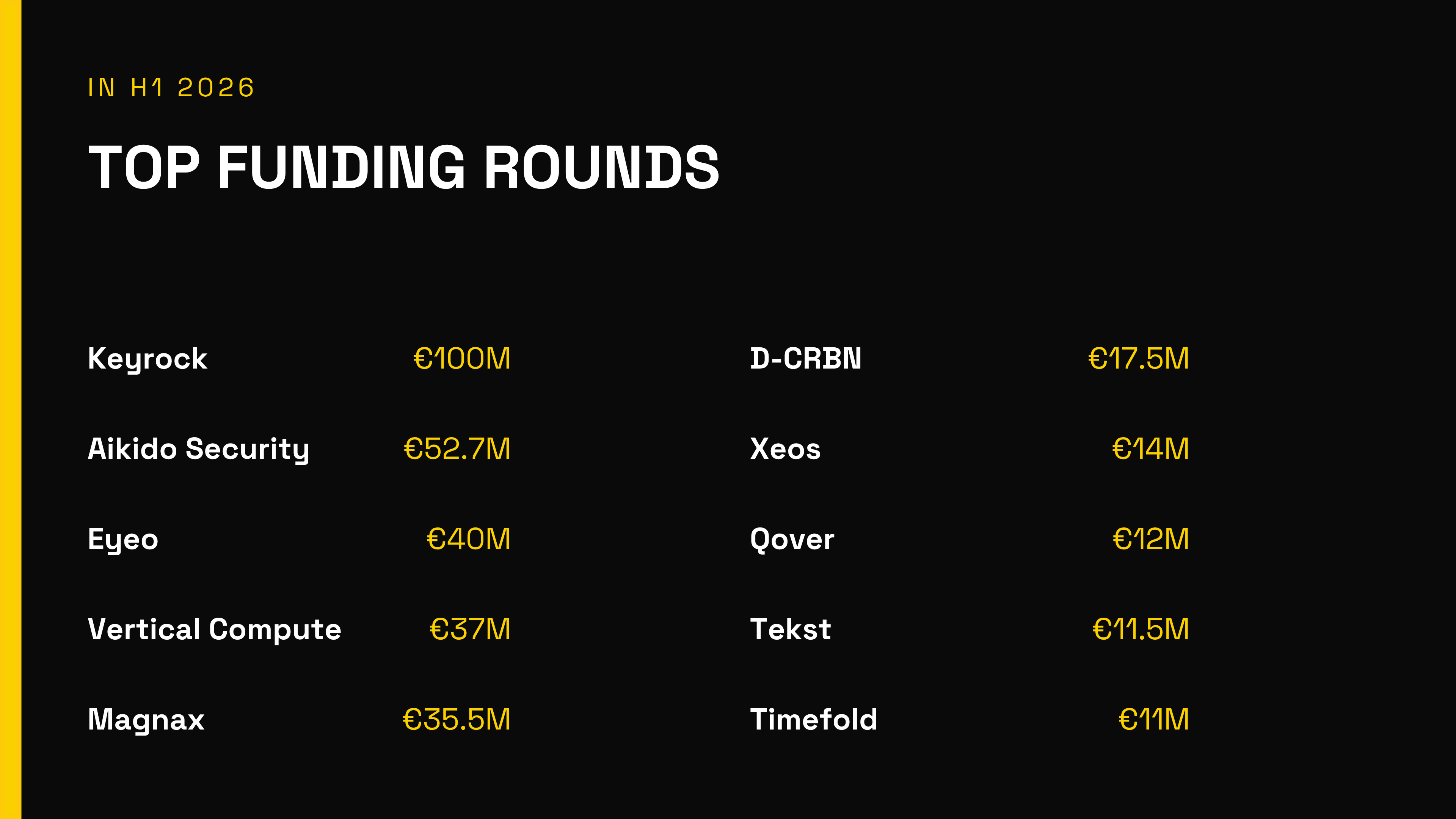

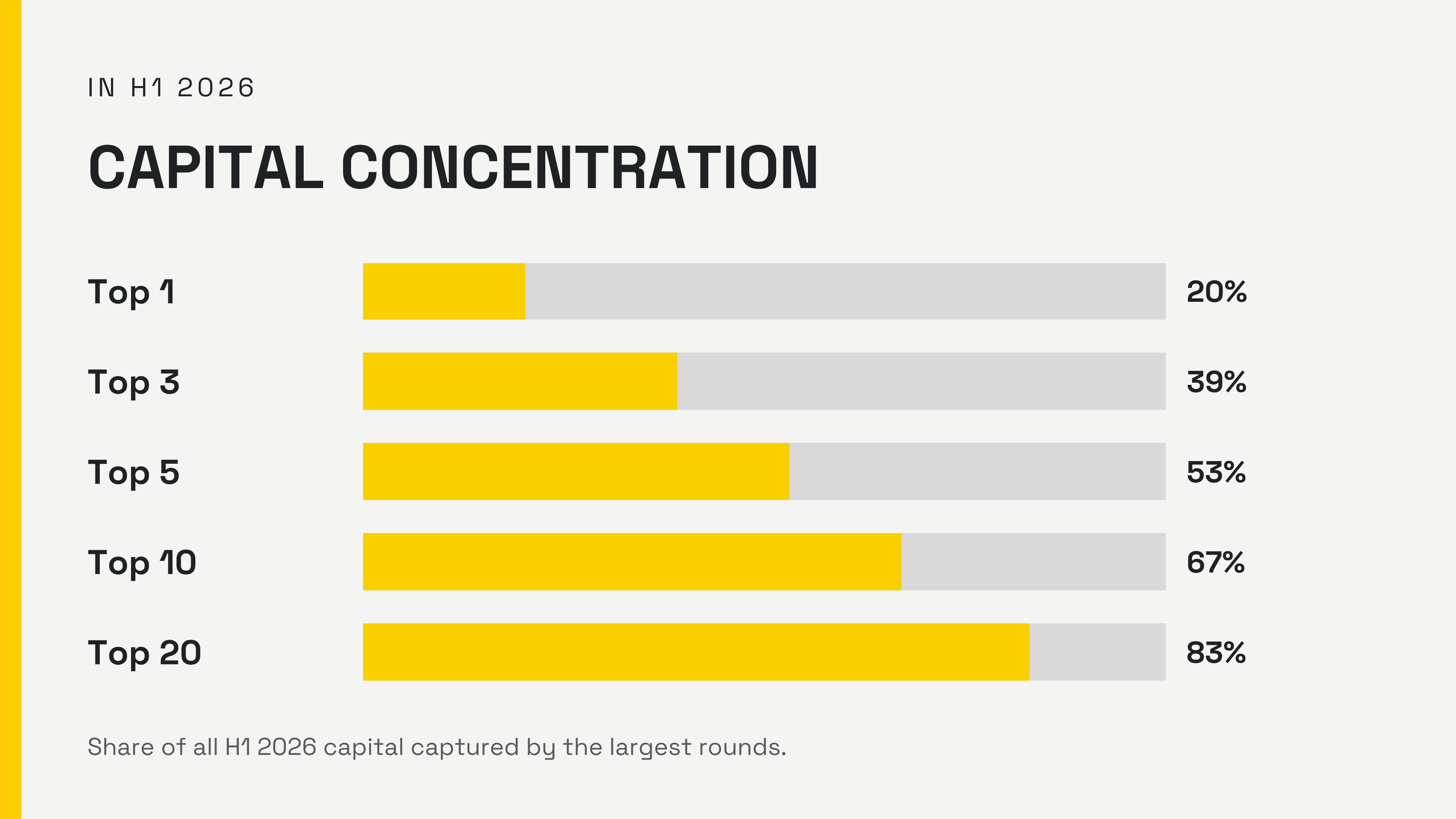

Belgian tech raised €497.1M in H1 2026, up 40% on last year. But 83% of it went to just 20 rounds.

More money to fewer companies: capital concentration in Belgian tech

The headline number (€497.1M) grabs attention, but the real story sits underneath.

The number of rounds barely moved, from 72 in H1 2025 to 74 in H1 2026. But the average round jumped 34%, to €6.7 million, while the median round actually fell 20%, to €1.6 million. More capital flowed, but it pooled around a smaller group of companies. Investors are writing bigger cheques to fewer names, the ones that already show commercial traction, international pull and capital efficiency.

This market runs on conviction, not abundance.

You see it in the numbers. The top five rounds pulled in 53 percent of all capital this half. The top twenty took 83 percent. That kind of concentration is the story of the Belgian venture in 2026: it's starting to look like growth-stage investing everywhere else, doubling down on proven quality instead of spreading thin across experiments.

The Series A gap is closing in Belgium. Now, scale-up financing is the new bottleneck

Here’s the part that matters most for what comes next.

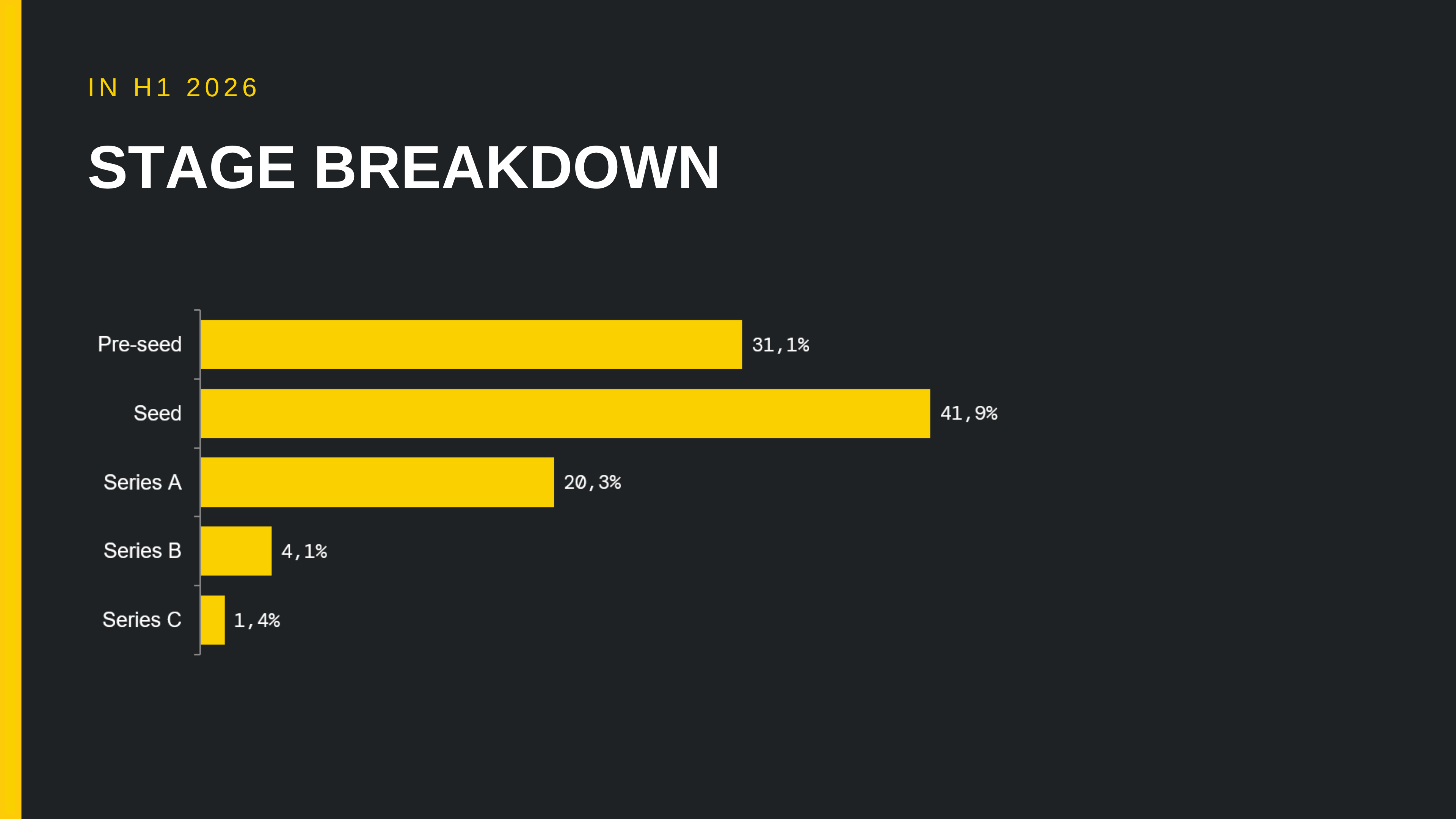

Series A has come back. It's one of the healthiest stages in the Belgian market right now, which would have sounded almost implausible a couple of years ago. But growth financing, the Series B and beyond that carries a company from "scaling" to "global," has become the new bottleneck. The Series A funding gap that defined Belgian tech for years is easing. Scale-up financing is where founders now hit the wall. The hardest part of building in Belgium is no longer getting to Series A. It's everything after.

This is the question every LP and policymaker should sit with. Belgium has shown, again and again, that it can produce tech companies the world wants. What it hasn’t cracked yet is keeping enough of them independent long enough to become global leaders instead of acquisition targets.

Belgium’s technology identity: where software meets engineering

Ask what Belgium is actually good at, and H1 2026 gives a sharper answer than you’d have gotten a few years back.

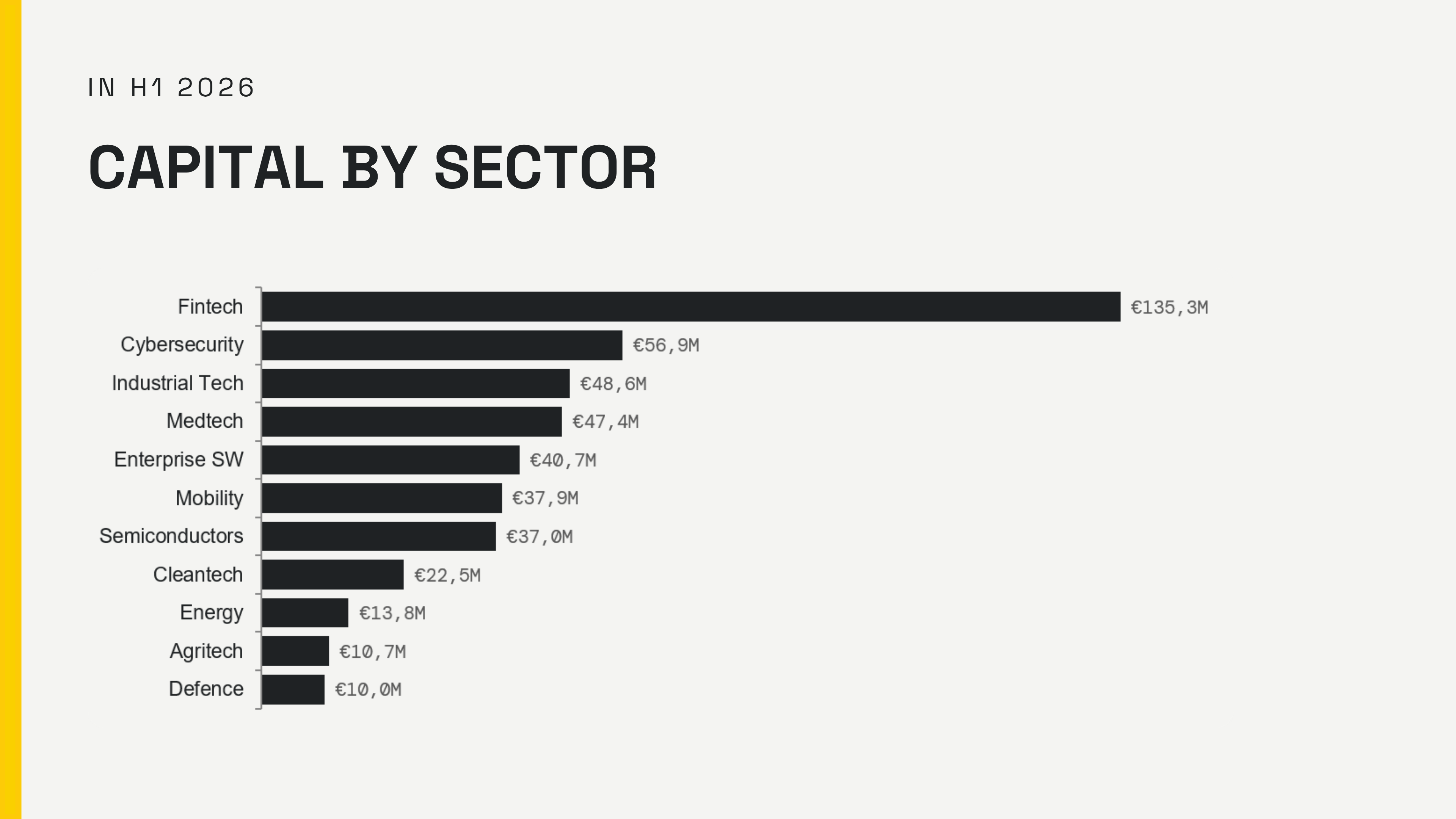

This isn’t a consumer-app ecosystem. Look at the biggest rounds, and you’ll find fintech, cybersecurity, photonics, industrial software, medtech, and climate. Business-to-business tech solving hard, defensible problems. Consumer apps barely show up in the top twenty.

More than half of all funding deals now have an AI angle, but Belgian AI isn’t a category in its own right. It’s a layer inside everything else: embedded in cybersecurity, industrial software, healthtech, and manufacturing. Belgium is playing in the space where software meets engineering, building an industrial AI and deep tech identity that aligns with Europe’s push for industrial competitiveness and tech sovereignty.

Filip Schouwenaars, a software engineer at Conveo and a Syndicate One member, put the shift in stark terms on our podcast. Most of what you build to automate a task today, he pointed out, gets recycled within three to six months as the models improve. The technical edge is real, but temporary. Which means the durable advantage moves elsewhere: to distribution, to customer relationships, to the parts of a business that compound.

The funding data says the same thing from another angle. As building software gets faster and cheaper, commercial execution isn’t the boring part anymore. It’s the moat.

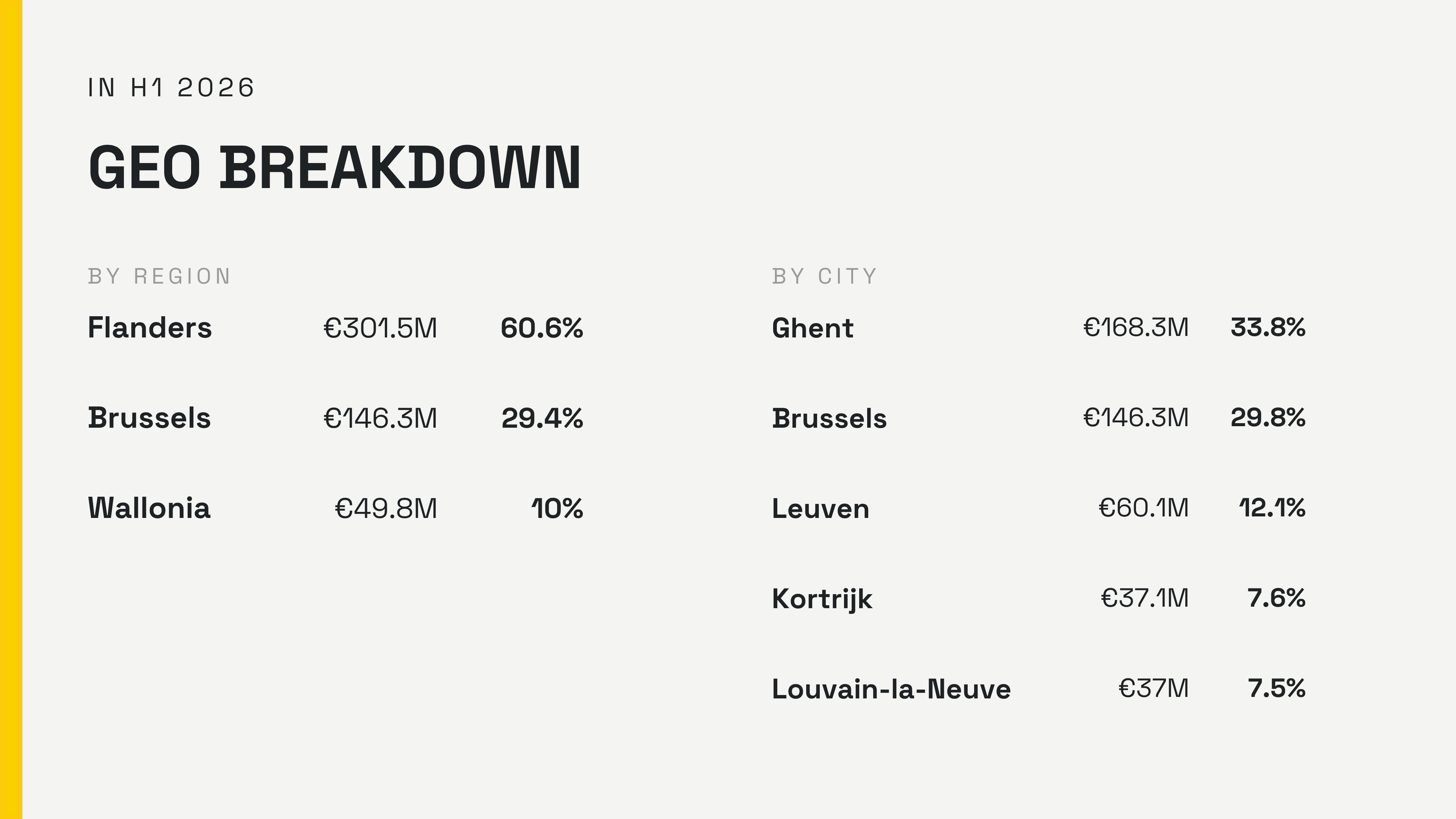

Belgian tech is a network, not a capital

Belgium doesn't really have a single startup city, and H1 2026 suggests that's a strength, not a weakness.

Flanders remains the broadest base at €301.5 million. Brussels pulls the big international rounds at €146.3 million. Wallonia keeps turning science into deeptech companies. At the city level, Ghent has quietly become the country’s strongest scale-up ecosystem, taking a third of all national funding, while the Leuven deeptech cluster stays one of Europe’s serious ones.

Most European countries rely on a single dominant hub. Belgium spreads its bets across several complementary ones, each with its own specialism. That diversity is a hedge: when one sector cools, the whole ecosystem doesn’t catch a cold.

Belgian startup exits in 2026: acquired for engineering, not market share

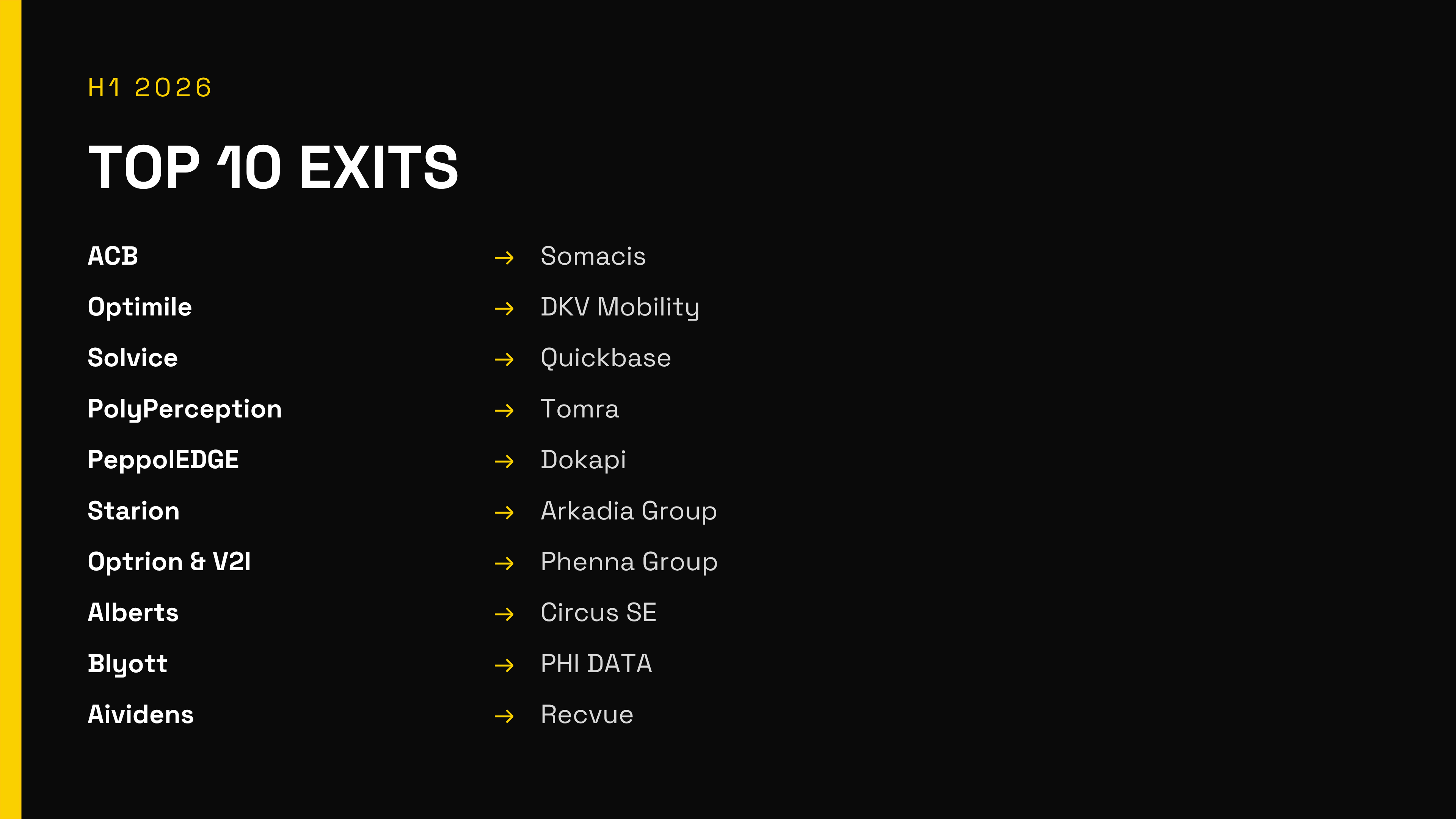

Funding took the spotlight in H1 2026, but the exit market remained active, with roughly 31 technology product exits over six months, most of them strategic acquisitions by international buyers.

Read those deals closely, and a pattern emerges. Buyers aren’t acquiring Belgian companies for market share. They’re acquiring engineering capability, specialized IP, and technical teams. Somacis bought ACB for semiconductors. Tomra bought PolyPerception for recycling AI. Quickbase bought Solvice for planning software.

It’s a compliment and a warning in the same breath. Belgium is very good at building companies the world wants to own. The open question, the one this report keeps returning to, is how many of them can stay independent long enough to become the ones doing the acquiring.

What H1 2026 actually tells us

Strip it back, and the half delivers one clear message: Belgium’s tech ecosystem has entered a more mature phase.

The companies raising are ones with deep technical expertise, real commercial traction, and international ambition. The buyers circling recognize exactly the same qualities. Both signals point the same way, toward genuine quality.

But the data also plainly names Belgium’s next job. Creating great companies is no longer the constraint. Keeping them, scaling them at home, turning more of them into global leaders, that’s the work ahead. It’ll take larger domestic growth funds, sustained international participation, stronger corporate-startup collaboration, and a culture that rewards founders for scaling independently rather than selling early.

H1 2026 wasn’t just a strong funding semester. It was a preview of a distinctive Belgian position, built on engineering, science, and industry. The next phase depends as much on commercial scale as on technical excellence.

If you're building toward that, you know where to find us. 🇧🇪

By Syndicate One, with Frederik Tibau: Expert Digital Innovation & Growth at Agoria, and a Syndicate One member.

Frequently asked questions

How much did Belgian startups raise in H1 2026?

Belgian tech companies raised €497.1 million across 74 disclosed funding rounds in the first half of 2026, up 40% on H1 2025.

Is the Series A funding gap in Belgium closing?

Yes. Series A is now one of the healthier stages in the Belgian market. The bottleneck has shifted to scale-up financing, the Series B and growth rounds that carry a company from scaling to global.

Which sectors attract the most funding in Belgium?

Fintech led H1 2026 at €135.3 million, followed by cybersecurity, industrial technologies, medtech, and enterprise software. More than half of all deals had an AI component.

Which Belgian cities raise the most startup capital?

Ghent led at €168.3 million (a third of national funding), ahead of Brussels and Leuven. Flanders took 60.6% of the capital by region, Brussels 29.4%, and Wallonia 10%.

Why do Belgian startups get acquired early?

International buyers increasingly acquire Belgian companies for their engineering capability, specialized IP, and technical teams rather than market share. The ecosystem’s next challenge is helping more companies stay independent long enough to become global leaders.

Methodology note: the H1 2026 figures are drawn from the State of Belgian Tech research, produced by Syndicate One together with Agoria and Scaleup Flanders, who partner on this analysis this year.

.svg)